Silicon Valley Bank SVB collapse explainer startups venture capital. The sudden failure of Silicon Valley Bank (SVB) sent shockwaves through the startup community and venture capital world. This explainer dives deep into the events leading to the collapse, analyzing the immediate and long-term impacts on startups and investors. We’ll examine the role of the Federal Reserve, explore alternative funding sources, and discuss the future of venture capital in light of this crisis.

The collapse exposed vulnerabilities in the banking sector’s handling of tech company deposits and investment strategies. The ensuing ripple effects on startups highlighted the importance of diversification and preparedness for unexpected economic shifts. This analysis provides a comprehensive understanding of the crisis, offering insights into potential solutions and lessons learned.

Overview of the Silicon Valley Bank (SVB) Collapse

The sudden collapse of Silicon Valley Bank (SVB) in March 2023 sent shockwaves through the financial world, particularly impacting the tech startup community. This catastrophic event exposed vulnerabilities in the banking sector and highlighted the interconnectedness of the economy. The fallout from SVB’s demise had far-reaching consequences, affecting not just startups but also venture capital firms and the broader financial ecosystem.

Summary of the SVB Collapse

SVB, a prominent bank catering to the technology sector, experienced a rapid and dramatic decline. A significant portion of its assets were invested in long-term U.S. Treasury bonds and mortgage-backed securities. However, the rising interest rates and subsequent decline in the value of these assets created a liquidity crisis. SVB’s exposure to the tech sector, particularly startups, proved to be a critical factor.

Many startups had deposited large sums of capital with SVB, creating a dependency and, ultimately, a vulnerability when the bank faced financial strain. The bank’s failure triggered a chain reaction, causing a ripple effect throughout the venture capital and startup communities.

Immediate Impact on the Banking Sector and Broader Economy

The collapse of SVB immediately triggered a wave of uncertainty and fear within the banking sector. Deposits from other banks and institutions were withdrawn in anticipation of similar failures, leading to a potential liquidity crisis. The situation heightened concerns about the stability of the broader financial system. The collapse also had significant implications for the broader economy, potentially impacting consumer confidence and investment activity.

The swift response by regulators and the Federal Deposit Insurance Corporation (FDIC) was crucial in preventing a larger financial crisis.

Ripple Effects on the Startup Ecosystem

The failure of SVB had profound consequences for the startup ecosystem. Many startups relied on SVB for banking services, including deposit accounts and loans. The closure of the bank created a significant disruption in funding and operational activities for these companies. Venture capital firms were also impacted, as many had invested funds through SVB, leading to potential losses and adjustments in investment strategies.

The crisis highlighted the vulnerability of startups to unexpected banking failures and the importance of diversification in financial strategies.

The Silicon Valley Bank (SVB) collapse is a significant event for startups and venture capital. Understanding the explainer helps us see the ripple effects. A crucial aspect of data storage for drone operations, like those using a Seagate DJI Fly Drive, is the crucial role of reliable hard drives and micro SD cards. The need for robust storage solutions, like those available in the seagate dji fly drive drone micro sd card hard drive category, is undeniable, and this highlights the broader implications of the SVB crisis for the future of startups and venture capital.

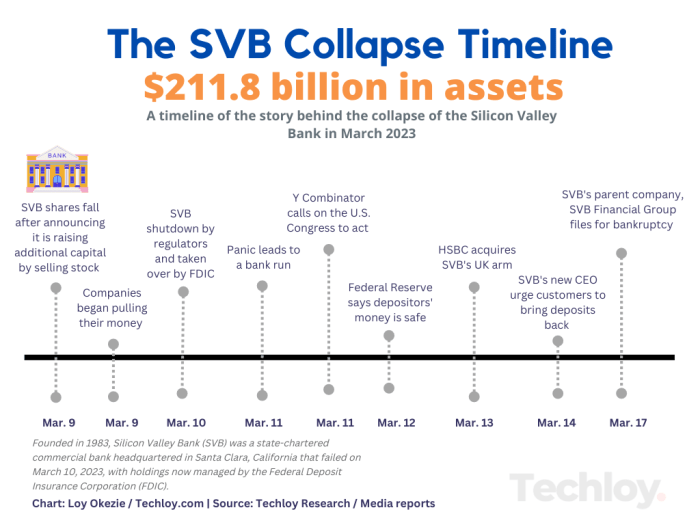

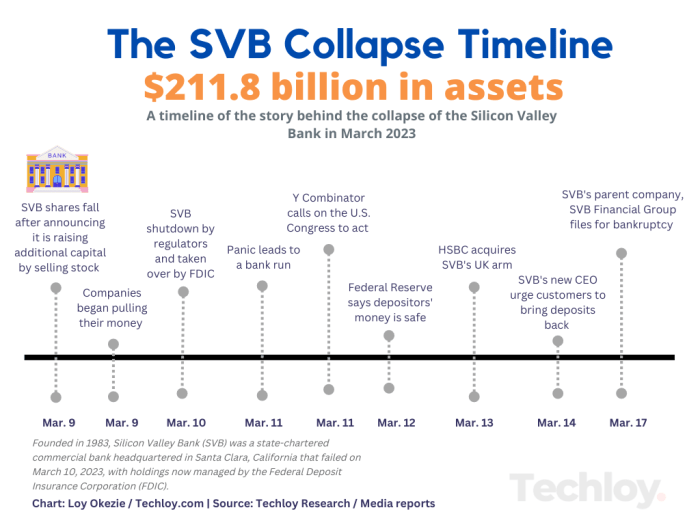

Timeline of Key Events

| Date | Event | Description | Impact on Startups |

|---|---|---|---|

| March 9, 2023 | SVB Announces Reduced Valuation | SVB disclosed significant unrealized losses on its bond portfolio. | Initial concerns regarding SVB’s financial health were raised. |

| March 10, 2023 | SVB Shares Plummet | Significant declines in SVB’s stock price fueled fears of a broader banking crisis. | Startups holding accounts at SVB experienced significant anxieties. |

| March 10, 2023 | Federal Reserve Steps In | The Federal Reserve announced measures to stabilize the banking system. | Investors and startups found some relief from the situation. |

| March 13, 2023 | SVB Closed by FDIC | The FDIC took control of SVB, guaranteeing customer deposits. | Many startups experienced a significant disruption in their operations, funding, and financial planning. |

Understanding the Causes of the Collapse

The sudden and dramatic collapse of Silicon Valley Bank (SVB) sent shockwaves through the financial world. This wasn’t just a localized banking issue; it exposed vulnerabilities in the entire system and raised critical questions about banking regulations and investment strategies. The investigation into the factors leading to SVB’s failure reveals a complex interplay of macroeconomic forces, risky investment practices, and perhaps a gap in regulatory oversight.

The Role of Federal Reserve Interest Rate Hikes, Silicon valley bank svb collapse explainer startups venture capital

The Federal Reserve’s aggressive interest rate hikes in 2022 significantly impacted SVB’s profitability and solvency. These increases led to a substantial decline in the value of SVB’s bond portfolio. As interest rates rose, the market value of bonds SVB held, particularly those with fixed interest rates, decreased. This meant that the bank’s assets were worth less than their book value, a crucial indicator of financial health.

The mismatch between the fixed-income assets and the variable-income liabilities proved to be a critical factor in the bank’s liquidity crisis.

SVB’s Exposure to Tech Company Deposits and Investment Strategies

SVB’s business model heavily relied on deposits from technology companies. This reliance created a vulnerability to market fluctuations. The rapid growth of the tech sector, particularly in the years prior to the collapse, had attracted a significant amount of deposits from startups and venture capital firms. This large pool of deposits, often characterized by a high concentration of assets and high turnover, proved difficult to manage in the face of changing market conditions.

SVB’s investment strategy, particularly its substantial holdings of long-term bonds and other fixed-income securities, also played a role. The rapid rise in interest rates made these assets less valuable, leading to a decline in their market value. Furthermore, SVB’s investment strategy prioritized preserving capital over maximizing returns, potentially exposing it to risks associated with market volatility.

The Role of Banking Regulations in Preventing Similar Events

The events surrounding SVB’s collapse highlighted potential weaknesses in banking regulations. While the Federal Deposit Insurance Corporation (FDIC) provides insurance for deposits up to a certain amount, the failure of SVB underscores the need for more robust regulations. The scrutiny of regulations and capital requirements could prevent banks from taking on excessive risk. Moreover, the need for stricter oversight of banks’ investment strategies, especially in the context of volatile market conditions, was also brought into sharp focus.

Comparison with Other Banks Facing Similar Challenges

While SVB’s collapse was unique, other banks, particularly those heavily invested in the tech sector, faced similar challenges. The rise in interest rates impacted the profitability of banks holding substantial fixed-income portfolios. However, the combination of factors that led to SVB’s downfall, including its specific investment strategy, reliance on tech company deposits, and the timing of the interest rate increases, was likely unique.

The situation underscores the need for a holistic approach to understanding and mitigating financial risks in the banking sector.

Factors Contributing to the SVB Collapse

| Factor | Explanation | Impact on SVB | Mitigation Strategies |

|---|---|---|---|

| Federal Reserve Rate Hikes | Significant increases in interest rates decreased the market value of bonds held by SVB. | Reduced asset value, leading to a loss of capital. | Diversification of investment portfolios, including a greater proportion of assets with varying interest rate sensitivities. |

| Exposure to Tech Company Deposits | Heavy reliance on deposits from tech companies, especially startups and venture capital firms. | High concentration of deposits susceptible to market fluctuations and withdrawals. | Implementing robust risk management strategies to monitor and mitigate the impact of high-concentration deposits. |

| Investment Strategies | Prioritizing capital preservation over maximizing returns with significant holdings in long-term bonds and fixed-income securities. | Vulnerable to interest rate fluctuations, potentially leading to significant losses. | Developing a more dynamic investment strategy that adjusts to market conditions and incorporates a higher proportion of assets with greater liquidity. |

| Banking Regulations | Potential gaps in regulatory oversight and capital requirements. | Increased risk of financial instability if not adequately addressed. | Strengthening banking regulations, particularly those related to risk management and capital adequacy, to prevent similar situations. |

Impact on Startups and Venture Capital

The sudden collapse of Silicon Valley Bank (SVB) sent shockwaves through the startup ecosystem and venture capital world. The bank’s failure exposed vulnerabilities in the financing landscape and forced startups to reassess their funding strategies, highlighting the interconnectedness of the financial system and the entrepreneurial world. This crisis underscored the need for diversification in funding sources and more robust risk management strategies for both startups and investors.The collapse of SVB created a significant funding crunch for many startups that had relied heavily on the bank for deposits and loans.

The Silicon Valley Bank (SVB) collapse is a major event for startups and venture capital, highlighting the fragility of the financial system. Understanding the details is crucial, and there are plenty of explainer articles out there. However, this recent turmoil isn’t isolated. The Canadian Competition Bureau’s investigation into Google’s ad business, for example, demonstrates broader concerns about market dominance and its impact on innovation.

Ultimately, these interconnected issues force us to re-evaluate the entire ecosystem supporting startups and the financial risks they face.

This disruption had far-reaching consequences for the venture capital industry, impacting investment strategies and the overall funding environment. Startups at various stages of development faced unique challenges, with the severity of the impact varying depending on their reliance on SVB and their ability to adapt.

Impact on Startups Relying on SVB for Funding

SVB’s demise significantly impacted startups that held substantial deposits or had outstanding loans with the bank. Sudden account closures and loan unavailability created immediate cash flow problems, jeopardizing ongoing operations and potentially forcing some startups to cease operations or seek alternative financing. The lack of readily available funding affected startups across diverse sectors, from tech companies to biotech firms, and significantly impacted their ability to execute their business plans.

Many startups had to scramble to find alternative funding sources, often with limited options and at less favorable terms.

Challenges Faced by Startups Due to the Collapse

The collapse presented several key challenges for startups. First, the immediate loss of access to funds severely hampered operational activities. Startups that were reliant on SVB for working capital experienced disruptions in their daily operations, impacting everything from payroll to inventory management. Second, the uncertainty surrounding the financial market created a climate of anxiety, further complicating fundraising efforts.

Investors were hesitant to commit capital, leading to a contraction in the overall funding environment. Third, startups had to quickly reassess their financial strategies, exploring alternative funding sources, such as other banks, venture capital firms, or crowdfunding platforms. The speed and scale of this adjustment were often critical to survival.

Implications for Venture Capital Firms and Their Investment Strategies

The SVB collapse had a substantial impact on venture capital firms. Many firms held significant portfolios of investments, and the failure of SVB directly impacted their holdings. The collapse underscored the need for diversification in funding strategies, including diversifying their portfolio companies’ funding sources. It also prompted a review of risk management practices within the venture capital sector.

Firms needed to evaluate their portfolio companies’ reliance on specific financial institutions and implement contingency plans for potential disruptions. This included a greater emphasis on assessing the financial health of the institutions supporting their portfolio companies.

The Silicon Valley Bank (SVB) collapse has understandably shaken up the startup and venture capital world. It’s a complex issue, and understanding the explainer pieces is key for anyone following the sector. Protecting your investments, and your devices, is also important. For a top-tier selection of screen protectors for your Motorola Edge, check out this helpful guide on best Motorola Edge screen protectors.

Ultimately, navigating the post-SVB landscape requires careful consideration, and staying informed about market trends remains crucial for anyone involved in startups and venture capital.

How the Collapse Influenced the Funding Environment

The SVB collapse significantly influenced the funding environment for startups. The event triggered a period of heightened uncertainty and caution in the market, leading to a contraction in funding availability. Investors became more discerning in their investment decisions, demanding more robust financial projections and risk assessments from startups seeking funding. The collapse highlighted the interconnectedness of the financial system and the importance of robust risk management for all parties involved.

Venture capital firms were compelled to reassess their investment criteria, with a stronger emphasis on evaluating the financial health of the institutions supporting their portfolio companies.

Startup Funding Impact Assessment

| Startup Stage | Funding Source | Impact | Mitigation Strategies |

|---|---|---|---|

| Seed | Angel Investors, Seed Funds | Limited immediate impact, but potential for reduced investment appetite due to broader market uncertainty. | Strengthening relationships with existing investors, exploring alternative funding sources (e.g., crowdfunding). |

| Series A | Venture Capital Firms | Significant impact on funding rounds, potentially leading to delays or reduced investment amounts. | Diversifying funding sources, demonstrating a robust financial model and business plan, highlighting strong management team. |

| Series B & Beyond | Venture Capital Firms, Public Markets | Potentially facing difficulties in securing further funding or in accessing public markets, depending on their relationship with SVB. | Strengthening financial position, exploring strategic partnerships, or seeking acquisition opportunities. |

| Established | Debt financing, Public Markets | Potential disruptions to debt financing, but generally less immediate impact. | Diversifying debt financing sources, exploring alternative financing models, and ensuring sufficient liquidity reserves. |

Long-Term Implications and Lessons Learned

The Silicon Valley Bank (SVB) collapse sent shockwaves through the financial world, exposing vulnerabilities in the banking system and the startup ecosystem. The fallout highlighted critical weaknesses in risk management, investment strategies, and regulatory oversight. Understanding these long-term implications is crucial for building a more resilient financial landscape and fostering a healthier startup environment.

Effects on the Financial Sector

The SVB collapse underscored the interconnectedness of the financial system. The bank’s failure triggered a chain reaction, impacting other institutions and investor confidence. This demonstrated the need for robust stress tests and contingency plans to mitigate systemic risk. Furthermore, the event spurred discussions about the appropriate level of regulation for banks specializing in specific sectors, like the tech industry.

The fragility of banks with concentrated exposures and the potential for contagion effects within the financial sector became more evident.

Impact on the Startup Community

The SVB collapse directly impacted startups reliant on the bank for their funding and financial services. Many startups experienced significant disruptions in their operations, including cash flow issues and difficulties accessing capital. This event highlights the importance of diversifying funding sources and having backup plans in place to navigate unforeseen financial shocks. The collapse also brought into sharper focus the importance of understanding the risks associated with deposit concentration in a single institution.

Regulatory Changes and Their Impact

The SVB collapse is likely to lead to stricter regulations regarding capital requirements, liquidity management, and risk assessment for banks serving specialized sectors. These changes are intended to bolster the stability of the banking system and prevent future crises. The future of banking will likely involve a more stringent regulatory environment, potentially affecting the lending practices of banks serving startups and venture capital firms.

Diversification in Investment Strategies

The SVB collapse serves as a stark reminder of the importance of diversification for startups and venture capital firms. Over-reliance on a single funding source or investment strategy can leave entities vulnerable to unexpected shocks. Startups and investors should actively seek multiple funding channels and diversify their investment portfolios to reduce their exposure to individual institutions or markets.

Examples include exploring alternative lending options, investing in diverse startups, and employing a mix of debt and equity financing strategies.

Comparison with Past Financial Crises

The SVB collapse shares some similarities with past financial crises, such as the 2008 financial crisis. Both events highlighted the dangers of unchecked risk-taking and the importance of robust regulatory oversight. However, the specific triggers and mechanisms differed, highlighting the evolving nature of financial risk in the modern era. Comparing the SVB collapse with past crises offers valuable insights into recurring patterns and potential preventative measures.

Table: Analyzing the SVB Collapse

| Factor | Impact | Potential Solutions | Lessons Learned |

|---|---|---|---|

| Concentration Risk | SVB’s concentration in a single sector (startups) amplified its vulnerability. | Diversification of customer base and asset types. Implementing more robust risk assessment models. | Over-reliance on a single sector or customer segment is risky. Diversification is key to mitigating such risks. |

| Liquidity Risk | SVB’s inability to meet the demands of depositors led to a run on the bank. | Enhanced liquidity management practices, stress testing, and contingency planning. | Banks need to maintain adequate liquidity reserves and have clear plans for managing large withdrawals. |

| Regulatory Gaps | Insufficient regulatory oversight in the context of specialized banking services. | Strengthening regulations and supervision for institutions operating in specific sectors. | Regulations must be tailored to the specific risks posed by various banking segments. |

| Investment Strategy | Mismatches between deposit liabilities and risky assets contributed to the crisis. | Improved risk management frameworks and more prudent investment strategies. | Understanding the risks associated with different investment options is crucial. |

Alternative Funding Sources for Startups

The collapse of Silicon Valley Bank (SVB) sent shockwaves through the startup ecosystem, highlighting the critical need for diversification in funding strategies. Startups, especially those reliant on traditional bank loans, suddenly faced a significant funding gap. This necessitates exploring a wider array of alternative funding sources to ensure continued growth and resilience.

Angel Investors

Angel investors are high-net-worth individuals who provide seed funding and mentorship to early-stage startups. Their investment often comes with valuable industry connections and guidance. They typically focus on startups with a strong team and innovative business models, seeking high returns. A key benefit is the flexibility and tailored support offered, often tailored to the specific needs of a startup.

However, angel investors may have their own investment criteria and priorities, potentially creating a challenging selection process.

Venture Capital Firms

Venture capital (VC) firms are prominent players in the funding landscape. They invest in high-growth startups, often providing substantial capital for expansion and scaling operations. VC firms offer substantial funding, but their investment decisions are based on thorough due diligence and rigorous evaluation. Startups must meet specific criteria and demonstrate significant potential for substantial return to attract VC capital.

This can be a highly competitive process, with startups facing rejection. VC involvement often entails relinquishing a significant portion of ownership.

Crowdfunding Platforms

Crowdfunding platforms provide a means for startups to raise capital from a large number of individuals. This approach can be beneficial for startups with a compelling narrative and strong brand presence, seeking to tap into a broader pool of investors. Crowdfunding can be an effective way to generate awareness and validation for a product or service. However, the success rate is variable, depending on the platform and the nature of the campaign.

Significant marketing efforts are often required to generate interest.

Incubators and Accelerators

Incubators and accelerators provide structured programs designed to support early-stage startups. These programs typically offer mentorship, networking opportunities, and resources to help startups develop their business models. They can be especially beneficial for startups with limited resources, offering support beyond just funding. However, these programs often have specific criteria for participation, and the funding amounts may not be substantial compared to VC funding.

Government Grants and Subsidies

Government agencies often provide grants and subsidies to support startups in specific sectors or regions. These funding opportunities can be a significant advantage, reducing the financial burden on startups. However, competition for these grants is fierce, and eligibility requirements can be stringent. The process of applying and receiving funding can be time-consuming and complex.

Debt Financing Alternatives

Beyond traditional bank loans, alternative debt financing options are available, including:

- Peer-to-peer lending platforms: These platforms connect borrowers directly with individual investors, providing an alternative to traditional lenders. This can be a quicker and less bureaucratic way to secure funding. However, interest rates can be higher compared to traditional bank loans.

- Merchant cash advances: This involves receiving a lump sum of cash based on a percentage of future sales. While this can be a fast way to access funds, it can be a costly option with high interest rates.

- Equipment financing: This option is ideal for startups requiring specific equipment for operations. The financing is tied to the value of the equipment.

Private Equity

Private equity firms invest in established startups or companies looking to grow further. This funding can be substantial and often comes with strategic advice. However, the level of equity given up to the private equity firm can be substantial, and the process can be complex.

Bootstrapping

Bootstrapping is the practice of funding a startup using internal resources and revenues. This can be a viable option for startups with a strong focus on efficient resource management. This option allows startups to maintain complete control and avoid giving up equity. However, bootstrapping may restrict growth and necessitate a highly disciplined approach to operations.

Other Sources

- Friends and Family: This is a classic method, tapping into personal networks for initial funding. This approach can offer significant support, especially in the early stages. However, it can be challenging to scale and may limit growth potential.

- Revenue-Based Financing: This method allows startups to access funds based on a portion of their future revenue. This can be attractive to startups with predictable revenue streams. However, it can be complex to structure and negotiate.

Illustrative Case Studies of Startups Affected: Silicon Valley Bank Svb Collapse Explainer Startups Venture Capital

The Silicon Valley Bank (SVB) collapse sent shockwaves through the startup ecosystem, leaving many companies reeling from the sudden loss of access to crucial funding. This section delves into the experiences of several startups directly impacted by the crisis, highlighting the specific challenges they faced and the innovative strategies they employed to navigate the turbulent waters. Understanding these case studies provides valuable insight into the broader implications of the collapse and the resilience of the entrepreneurial spirit.

Case Study 1: A Biotech Startup Facing Clinical Trials

This biotech startup, focused on developing a new cancer treatment, had a significant portion of its capital locked in SVB accounts. The swift and unexpected closure of the bank meant the company faced an immediate liquidity crisis, jeopardizing its ability to fund ongoing clinical trials. Critical equipment, research materials, and personnel salaries were all at risk.

- Challenge: Sudden loss of readily available funds, inability to access critical capital for ongoing clinical trials, and the risk of halting critical research.

- Adaptation: The startup rapidly explored alternative funding options, including loans from specialized venture capital firms and government grants aimed at supporting biomedical research. They also initiated cost-cutting measures to extend their runway, including renegotiating contracts and exploring potential partnerships for research collaborations.

- Key Takeaway: The importance of diversification in funding sources and the crucial role of government support for critical research sectors in times of financial uncertainty.

Case Study 2: A SaaS Startup in the Expansion Phase

A software-as-a-service (SaaS) company, rapidly expanding its customer base and product offerings, had significant funds deposited in SVB. The bank’s failure meant the startup lost access to crucial operating capital, hindering its ability to scale operations. Recruitment of key personnel was also threatened.

- Challenge: Loss of operational capital, difficulty in securing new funding, and the threat of delays or setbacks in expansion plans.

- Adaptation: The company successfully negotiated loans with other financial institutions and sought assistance from industry associations. They also implemented stringent cost-cutting measures and prioritized securing alternative funding streams. They reassessed their business plan to ensure they were operating within their new financial realities.

- Key Takeaway: The necessity of a well-defined contingency plan and the value of industry support networks during financial crises.

Case Study 3: A Web3 Startup Reliant on Liquidity

A blockchain-based startup heavily reliant on the fluidity of the cryptocurrency market and SVB for their operational funding faced a significant setback. The bank’s closure meant a loss of access to liquidity and an inability to meet short-term financial obligations.

- Challenge: Sudden loss of access to liquidity and the difficulty of securing alternative funding in a volatile market environment.

- Adaptation: The startup explored alternative financial services, including cryptocurrency exchanges and decentralized finance (DeFi) platforms. They also restructured their business operations to minimize their reliance on traditional banking services.

- Key Takeaway: The importance of recognizing the potential risks of over-reliance on a single financial institution and the need to explore diverse financial options.

Future of Venture Capital in Light of SVB

The implosion of Silicon Valley Bank (SVB) sent shockwaves through the startup ecosystem, forcing a re-evaluation of risk and resilience in venture capital. Investors are now scrutinizing the financial health of their portfolio companies and re-assessing their investment strategies, leading to a more cautious approach to funding rounds. The crisis highlighted the vulnerabilities of a system heavily reliant on short-term deposits and exposed the need for greater diversification and financial preparedness in the startup world.The SVB collapse underscored the interconnectedness of the financial system and the potential for systemic risk within the venture capital industry.

Venture capitalists are adapting their strategies to mitigate these risks, prioritizing financial stability and operational resilience in their portfolio companies. This shift is likely to affect the startup landscape in several significant ways, influencing funding rounds, investment terms, and ultimately, the trajectory of innovation.

Investment Strategy Adjustments

Venture capitalists are now more likely to demand stronger financial statements and more detailed projections from startups seeking funding. This includes a deeper dive into cash flow management, contingency planning, and diversification of funding sources. They are also prioritizing startups with sustainable business models and strong revenue streams, moving away from those reliant on rapid growth fueled by short-term funding.

A significant trend involves exploring alternative funding models that reduce reliance on traditional banking institutions.

Response to the Changing Landscape

Venture capital firms are responding to the crisis by diversifying their investment strategies. This involves allocating a greater percentage of capital to companies with more established revenue models and predictable cash flows. Furthermore, many firms are actively seeking out alternative funding vehicles such as private credit and debt financing, providing additional avenues for startups. This approach offers a more balanced approach to risk management.

Additionally, venture capitalists are working closely with portfolio companies to develop comprehensive financial plans and ensure they are well-prepared for future economic uncertainties.

Potential Shifts in the Startup Ecosystem

The SVB collapse is likely to influence the startup ecosystem in several ways. Funding rounds might become smaller and more frequent, reflecting a more cautious approach to investment. Furthermore, investment terms could become more stringent, requiring startups to demonstrate greater financial stability and operational resilience. Startups might also be encouraged to explore alternative funding sources, potentially leading to a greater diversity of funding models and a more resilient startup ecosystem.

Impact on Funding Rounds and Investment Terms

The SVB collapse has significantly impacted funding rounds. Venture capital firms are likely to be more selective in their investments, focusing on startups with proven business models and strong revenue projections. Investment terms, including valuation multiples and preferred equity terms, are likely to reflect the current market environment, potentially leading to more cautious and realistic valuations.

Analysis of Venture Capital Adjustments

| Investment Strategy | Changes | Impact | Future Trends |

|---|---|---|---|

| Traditional Bank Funding | Reduced reliance, increased scrutiny of financial health. | Increased need for alternative funding, more stringent investment terms. | Shift towards alternative financing options (private debt, venture debt). |

| Portfolio Company Financial Planning | Emphasis on cash flow management, contingency planning, diversification. | Increased operational resilience, reduced risk for venture capital firms. | More detailed financial projections required, potential for smaller, more frequent funding rounds. |

| Investment Selection Criteria | Focus on sustainable business models, proven revenue streams. | Potential for reduced investment in high-growth, early-stage startups. | Greater emphasis on mature business models and established revenue streams. |

| Alternative Funding Sources | Exploration of private credit, debt financing, etc. | Increased options for startups, potentially lowering funding costs. | Greater diversification in funding models, more resilience for the startup ecosystem. |

Ending Remarks

In conclusion, the SVB collapse served as a stark reminder of the interconnectedness of the financial world and the startup ecosystem. The crisis underscored the importance of diversification, robust financial planning, and adaptable strategies for startups and venture capital firms alike. While the immediate aftermath was challenging, the lessons learned will hopefully lead to a more resilient and prepared future for the tech industry and the financial sector.